Most recent

Gavekal Research

The (Better) Case For European Banks

Tan Kai Xian, Cedric Gemehl

10 Aug 2026

After more than a decade in the wilderness, European bank stocks have now had four good years, outperforming their US counterparts since 2022 in US dollar terms. The question is whether this outperformance can continue. The short answer is yes. European bank stocks are no longer priced at distressed levels, but with the earnings outlooks for European and US banks both solid, there is still room for European valuations to improve compared with the US.

Gavekal Dragonomics

The Offshore Tax Grab

Xiaoxi Zhang, Christopher Beddor

10 Aug 2026

In recent months, many people across China have received a text message with a “friendly reminder” from their local tax bureau: that they must declare and pay taxes on all income from offshore assets. Xiaoxi and Christopher argue it’s clear that enforcement is tightening up as the tax authorities work to boost revenue, and the latest actions go beyond enforcing existing rules to change some long-accepted tax practices.

Gavekal Research

Geoeconomic Monitor: China’s AI Moonshot

Tom Miller, Tom Holland

7 Aug 2026

As Chinese artificial intelligence models begin to compete with US models in many real-world tasks, Beijing is determined to build an alternative to Washington’s emerging AI ecosystem. It is pledging to help countries in the Global South develop their own AI capabilities, leveraging its technological clout for commercial and geopolitical gain. China’s cheaper models will prove popular but only if Beijing can maintain its commitment to “openness,” writes Tom Miller. Meanwhile, Tom Holland argues that Iran is attempting to drive a wedge between the US and the Gulf Arab states as it seeks to become the regional hegemon

Gavekal Research

The Scott Bessent Scorecard

Louis-Vincent Gave

7 Aug 2026

US Treasury Secretary Scott Bessent’s decision to help the Japanese Ministry of Finance prop up the yen may seem incongruous. After all, for a US Treasury secretary to willingly and very visibly buy the yen is essentially sending out a message to investors of “do not buy US treasuries; buy JGBs instead," while Japan is the largest foreign holder of US government bonds. So why would Bessent openly invite Japanese investors to turn tail?

Gavekal Dragonomics

How Anti-Corruption Threatens Investment

Christopher Beddor

State Subsidies Subside Further

Thomas Gatley

Macro Update: Pushed And Pulled

Wei He, Dragonomics Team

Consequences Of The Tech IPO Boom

Thomas Gatley

The Next Challengers In Memory Chips

Tilly Zhang

Gavekal Research

Video: China’s K-Shaped Economy

Tom Miller

A Shifting Global Currency Landscape

Louis-Vincent Gave, Romain Metivet

Europe’s Broad Earnings Recovery

Cedric Gemehl, August Gudmundsson

The RBI Hopes For The Best

Udith Sikand, Tom Miller

Should Equity Investors Be Reassured By Record Corporate Profits?

Anatole Kaletsky

Gavekal Technologies

China’s Export Engine Meets Europe’s Carbon Rules

AJ Cortese

On The Ground At The 2026 World AI Conference (Part II)

Laila Khawaja, Huang Shichan

What Just Happened, Kimi?

Laila Khawaja, Arthur Kroeber, Tom Hancock

On The Ground At The 2026 World AI Conference (Part I)

Laila Khawaja, Huang Shichan

EVs’ Year Of Living Dangerously

AJ Cortese, Ernan Cui

Gavekal-IS

The Macroeconomics Of AI In Simple Terms

Didier Darcet

Currency Momentum Trading

Didier Darcet

The End Of The Risk-Free Asset

Didier Darcet

The Great Confusion Over Economic Quadrants

Didier Darcet

The Bond Portfolio For A Swiss Investor

Didier Darcet

Gavekal Research

Who Is Copying Who? Part IV

Louis-Vincent Gave

27 Jul 2026

The growing push to restrict Chinese AI models could mark a major escalation in US-China tensions—and a watershed for the US economy. Louis argues that a ban would protect US tech giants at the expense of start-ups, consumers and productivity, while accelerating the fragmentation of the global technology system. Over time, the result could be weaker US equities, a softer dollar and higher bond yields, raising the question of whether such a policy would truly serve the public good or merely entrench corporate power.

Checking The Boxes

Our short take on the latest news

Fact

Surprise

Takeaway

US nonfarm payrolls fell -23k MoM in Jul, versus 20k in Jun

Weaker than expected growth of 80k

Likely due to labor supply shortage; weak hiring and low firing environment persists

German industrial production rose 0.2% MoM in Jun, versus 0.7% in May

As expected; YoY, industrial production fell -0.1% in Jun, versus 0% in May

Transport equipment offsetting drop in machinery; output still on recovering trend

French unemployment rate rose to 8.3% in 2Q26, from 8.1% in 1Q26

Above expected 8.2%

Indicators point to continued gradual softening despite modest growth improvement

China's CPI rose 0.5% YoY in Jul, versus 1% in Jun

Inflation cooler than expected 0.8%; MoM, CPI fell -0.1%, versus -0.3%

Weak inflation suggests domestic demand remains sluggish

Test Your Knowledge

In July, the US announced a ban on imports of new humanoid robots made in China. What share of global humanoid robot sales did Chinese companies account for in 2025?

- 22%

- 44%

- 88%

- 99%

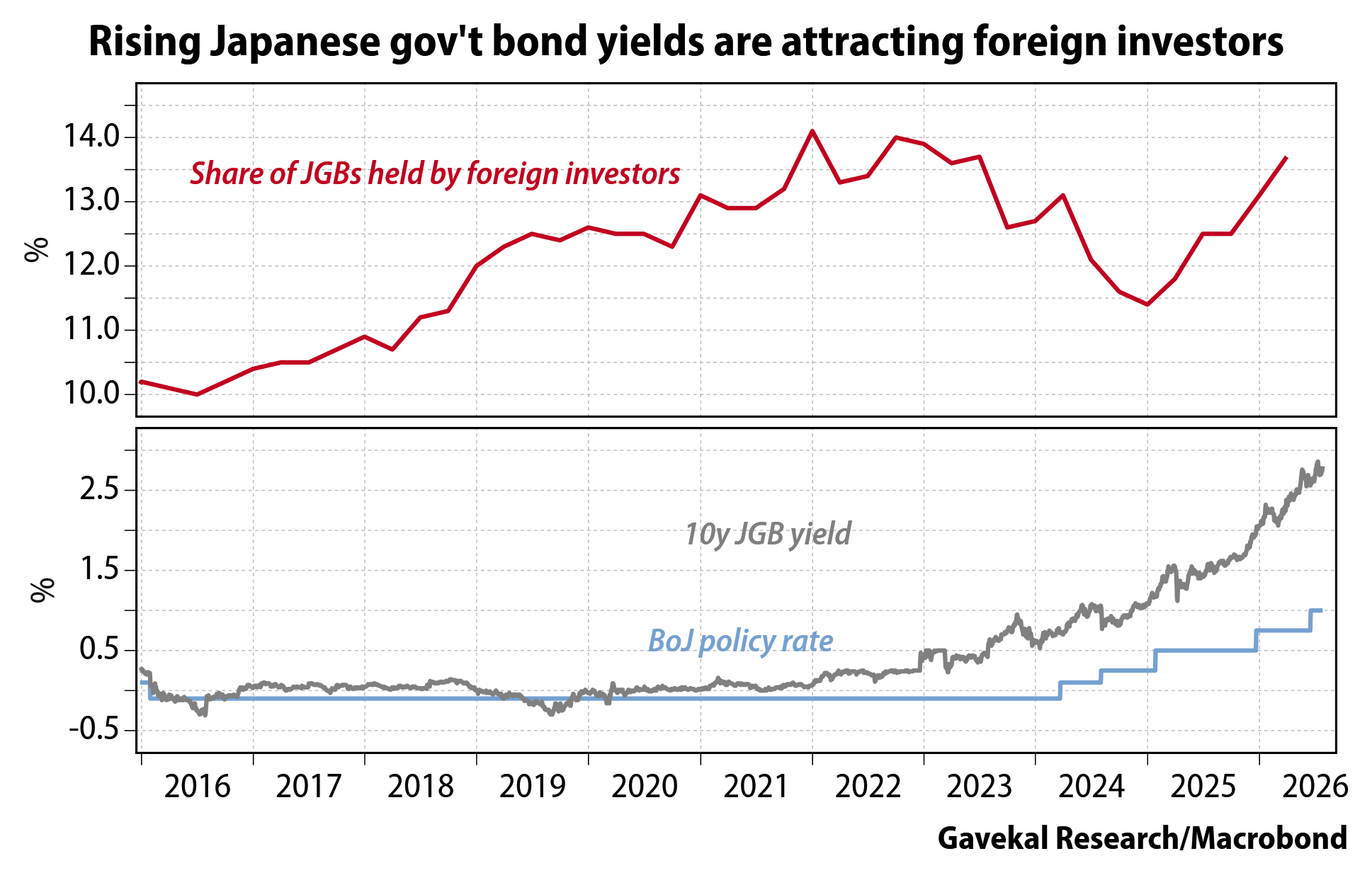

Chart of the Week

Rising bond yields and a weakening currency are usually a toxic combination for foreign investors. But over the past year, despite the yen’s weakness and a near-doubling of yields on the benchmark 10-year JGB, foreign investors have ramped up their holdings of JGBs. The main driver of this unexpected trend is the additional return generated from foreign exchange hedging costs for foreign investors—Japanese institutions have long been willing to pay a premium to borrow US dollars to hedge their overseas portfolios.

Open Chart

Gavekal Research

Essential Reading: A Book For Every Week Of The Year

Gavekal is often asked for a recommended reading list. So, here it is: a book a week that everyone interested in the world of macro investing—whether hoary veteran or eager apprentice—can benefit from reading.

Gavekal Research

Webinar: Regime Change Can Cause Market Madness

Anatole Kaletsky, Tom Holland

3 Jul 2026

Markets continue to behave as if the world has not fundamentally changed, even as inflation, interest rates, geopolitics and global capital flows enter a new regime. Anatole argues that investors are systematically mispricing four major shifts: the long-term outlook for inflation and bond yields, the global growth cycle, the rotation from AI-led growth to cyclical value and the end of US exceptionalism.

The Iran War And Fallout

Geoeconomic Monitor: Dominance And Decline

One upshot of the wars in the Persian Gulf and Ukraine is that the US oil and gas industry is booming. The drawback is that US consumers are paying twice Trump's target price for gasoline. With the midterms approaching, there is a risk the US administration might decide export controls are the only way to square the circle, writes Tom Holland. Meanwhile, Cedric Gemehl looks at how Germany is warming to the idea of protectionist measures to insulate its industries from Chinese competition.

The Energy Risk Remains (Part II)

The energy risk from the conflicts in the Middle East and Ukraine continue to escalate, and away from the limelight, listed pureplay oil refiners (outside of China and its price and export controls) have been having a monster year of their own, with recent gains starting to go parabolic. The obvious risk is that as crack spreads rise, so does the pressure on politicians to do something about the rising price of gasoline and diesel. So how can investors guard their portfolios against such risks?

The Energy Risk Remains (Part I)

Energy stocks, as a GICS sector, have delivered the best total return performance of any US sector over the past five years. Yet, tech stocks now account for almost 40% of the S&P 500’s market capitalization, while energy stocks—with their 3% weight—are close to record lows. So why are energy stocks so unloved, especially in the midst of an oil shock?

Geoeconomic Monitor: Latin America Turns Right

With tensions cooling in the Middle East, global attention is shifting elsewhere. In Latin America’s rambunctious political landscape, electorates continue to vote in right-wing leaders. But the wave may yet break before it reaches Brazil, where Luiz Inacio Lula da Silva is favorite to win his fourth term in October’s election, says Tom Miller. Back in the Strait of Hormuz, Tom Holland explains why Iran’s emerging protection racket sets a dangerous precedent for global trade.

US economy & markets

The (Better) Case For European Banks

After more than a decade in the wilderness, European bank stocks have now had four good years, outperforming their US counterparts since 2022 in US dollar terms. The question is whether this outperformance can continue. The short answer is yes. European bank stocks are no longer priced at distressed levels, but with the earnings outlooks for European and US banks both solid, there is still room for European valuations to improve compared with the US.

Bessent, The Yen And US Yields

Scott Bessent says he will do “whatever it takes” to help Japan prop up the ailing yen “in a way that helps the American economy.” The US Treasury secretary’s qualification is important. It strongly suggests that while the US administration wants the yen to appreciate, it very much does not want Japan to sell down any of its armory of US treasuries to fund interventions in the FX market. Will argues this points to another course of action for the US on the yen.

Five Ways The US Economy Depends On Higher Equity Prices

With market heavyweights like Nvidia down -12.3% from its early summer high, Micron down -31.7% and Oracle off -42.8%, it is remarkable that the broad S&P 500 closed on Monday down just -0.12% from its June 2 record. It is also an enormous relief for US policymakers, business

managers and consumers. This is because increasingly the health of the overall US economy is tied to the trajectory of the stock market. Where equity prices go, so goes US growth. There are at least five reasons for this.

Talky Talky

Kevin Warsh has promised to reshape the Federal Reserve, but after two meetings the institution looks very familiar. Will examines why the Fed chose to leave interest rates unchanged despite inflation remaining above target and argues that recent inflation data and tighter financial conditions gave policymakers room to wait rather than act. The key question for investors is whether this caution reflects a lack of resolve, or simply confidence that rates can still be raised later if inflation reaccelerates.

China chartbook

Gavekal Dragonomics

Macro Update: Pushed And Pulled

Wei He, Dragonomics Team

3 Aug 2026

China’s economy is being pushed and pulled by two external shocks: the supply shock from the Iran war and the demand shock from the AI capex boom. Both are creating lots of volatility in trade flows, prices and profits, although the underlying trend of the domestic economy has not yet changed much. Neither are China’s policymakers showing much sign of significantly changing course. In our latest quarterly chartbook, Wei and the Dragonomics team diagnose the current situation and the policy outlook.

India chartbook

Gavekal Research

India Macro Update: Downside Risks Abound

Udith Sikand, Tom Miller

23 Sep 2025

India’s domestic economic recovery is at risk as Prime Minister Narendra Modi’s government faces a lose-lose choice: continue to import cheap oil from its long-time ally Russia or face punitive tariffs in its biggest export market. Last week’s US interest rate cut will give the central bank more room to cut rates, but the underperformance of Indian asset prices looks set to continue.

Latest video

Gavekal Research

Video: China’s K-Shaped Economy

Tom Miller

6 Aug 2026

China’s economy slowed again in the second quarter, with little sign of domestic demand picking up. While traveling around China, Tom Miller found packed trains and tourist towns, but also complaints about low spending. For many, quality of life now appears to trump making money. Still, competition to provide goods and services remains brutal. And China’s high-tech economy keeps surging ahead, with monasteries in the mountains of Sichuan now receiving deliveries by drone.

Strategy Chartbook

Gavekal Research

Quarterly Strategy Review: 2Q26

Louis-Vincent Gave

3 Jul 2026

The second quarter was dominated by an extraordinary surge in risk appetite as semiconductor stocks powered one of the largest increases in global equity market capitalization on record, yet beneath the exuberance, markets underwent significant macro shifts. Louis reviews the quarter's defining developments.

Emerging markets

Video: Are EMs Back?

It’s been a good quarter for the broad emerging markets complex. The MSCI EM index has returned almost 7% in US dollar terms, while US equities are down by some -3.5%. So should investors jump on the EM train? Udith points out that there is a wide divergence in the performance of individual emerging markets, and the threat of tariffs hangs heavy over EM corporate earnings. Investors need to be selective.

Video: Southeast Asia Under Trump 2.0

Global investors are rightly focused on the potential losers from the United States pursuing an aggressively protectionist trade policy agenda, but there may be winners as well. Tom went in search of such economies last week. Today he explains how such “swing states” are likely to perform in an intensified period of great power rivalry between the US and China.

China Turbocharges EM Investment

As the rich world pulls up the protectionist drawbridge, investors risk missing a bigger story

in emerging markets. Here, Chinese outbound investment is rebounding after the fallow Covid years, and is driving a new wave of industrialization that promises to lower the cost of the green-energy transition.

Why This Time Has Been Different

During past episodes of risk-off volatility, the correlation between emerging market risk assets has shot up. But early August’s bout of market volatility saw a bifurcation in EMs, and no broader macroeconomic spillover effects—which speaks well of the growing maturity of emerging markets as an asset class.

Europe's economy

The (Better) Case For European Banks

After more than a decade in the wilderness, European bank stocks have now had four good years, outperforming their US counterparts since 2022 in US dollar terms. The question is whether this outperformance can continue. The short answer is yes. European bank stocks are no longer priced at distressed levels, but with the earnings outlooks for European and US banks both solid, there is still room for European valuations to improve compared with the US.

Europe’s Broad Earnings Recovery

Investors who question the sustainability of the AI earnings boom, but who nevertheless want to retain some exposure to the growth of artificial intelligence, may want to look again at European equities. Today, Europe offers a powerful earnings-recovery story, with a significant AI element. But best of all, the continent’s earnings growth is diversified across a broad range of sectors, and therefore stands a good chance of surviving even if the AI boom turns to bust.

Foreign Issuers Flock To Euro Debt

Record numbers of non-resident issuers are tapping the eurozone’s debt market in order to take advantage of favorable funding costs. But far from crowding out domestic borrowers, the influx of foreign issuers is deepening euro-denominated debt markets to the benefit of local issuers, writes August.

The Economics Of Wildfires And Heatwaves In Europe

Europe is facing an unprecedented combination of severe wildfires and extreme heat, raising questions about the macroeconomic consequences of climate-related shocks. Cedric argues that while wildfires have only a limited macroeconomic impact, heatwaves act as broader negative supply shocks by disrupting labor, food production, electricity generation and logistics. The result is another structural force making inflation above, rather than below, the ECB’s 2% target increasingly likely.

Currencies

Important Recent Developments

The Slump In Asian Currencies

A Concentrated Inflationary Boom Or A Bet On The Fed?

Demand And Supply Of Money

Dialing Back Expectations For Appreciation

Monetizing US Budget Deficits

Oil & commodities

Video: Towards An Uncertain Winter For Energy

The Quid Pro Quo That Wasn’t

The Energy Risk Remains (Part I)

Energy Markets Are Too Complacent

Video: Oil After Hormuz

The State Of World Oil Stocks