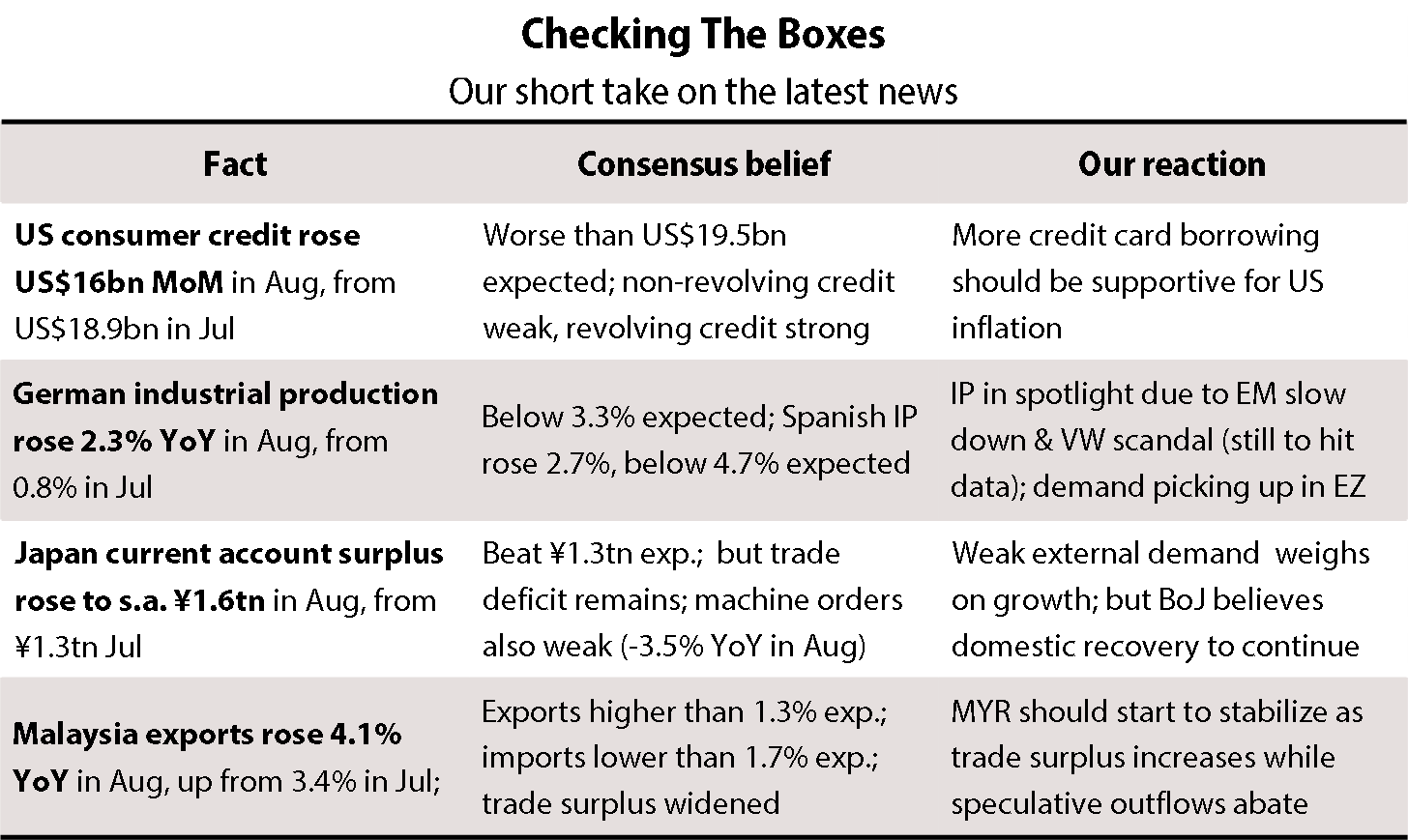

The most important financial news for months did not even get a mention in last night’s market reports from Bloomberg and Reuters. While the media scribes dutifully described the post-summer highs hit by Wall Street and several other markets, they attributed the revival of bullish spirits to rebounding commodity prices and energy and biotech shares—roughly equivalent to saying that markets went up because prices moved higher. Often such truisms are the only honest thing to say about a change in market sentiment, but this time there is a more interesting explanation, or more precisely three connected explanations:

- We have been telling clients for weeks that the most likely catalyst for a resumption of the bull market would be evidence that Beijing does not want any further significant devaluation of the renminbi over the coming months, and—even more importantly—proof that markets simply do not have the power to force a government with US$3.5trn in reserves to devalue against its will.

- The evidence against additional devaluation has been accumulating since mid-September, with anecdotal reports of diminishing capital outflows from China and of more genuine two-way trading in offshore and onshore renminbi. Yesterday Beijing published the reserve statistics that we have been waiting for. To our relief these showed a significantly smaller than expected reserve drain, confirming our suspicion that the capital flight out of China eased substantially after the feverish weeks immediately following the devaluation of August 11.

- If Chinese capital flight has died down, then the threat to the global economy generated by the summer turmoil has now lifted. Markets all over the world should therefore return to the risk-on mode that prevailed in the first half of the year.

Why was the threat of Chinese devaluation so important? Because the big problem this summer was not the state of the Chinese economy, which was only slightly weaker than expected. The real threat was a Lehman-style vicious circle in which weak economic data lead to collapsing financial confidence, causing policy mistakes which further damage the economy and financial confidence, giving the vicious circle another spin. Such vicious circles are most threatening if they create capital flight out of the currency or deposit flight from the banking system. In China’s case both could happen if a devaluation got out of control. That is why the small August devaluation caused much more financial angst around the world than July’s huge crash in the stock market.

What did we learn yesterday? The People’s Bank of China foreign reserves report showed a much smaller fall than expected—of only US$43bn in September, compared with a consensus estimate of US$57bn and a record fall of US$94bn in August. Considering that the first week of September saw heavy PBOC intervention, coinciding with a renewed sell-off in many Asian markets, the reserve drawdown required to stabilise the renminbi must have been quite modest in the past few weeks.

Does the end of Chinese devaluation fears justify a return to the risk-on strategies that worked so well in the first half of 2015? There is a range of views within Gavekal. Charles remains bearish about equities and credit because of his concerns about a US recession and global deflation. By contrast, I believe that the risk-on conditions earlier this year were justified by four or five strongly expansionary forces:

- Solid if unspectacular US growth, now driven by rising employment and incomes, not just by monetary stimulus;

- Mario Draghi’s enormous quantitative easing program, which has effectively guaranteed the eurozone against fiscal and banking problems for the next two years;

- US$2trn in annual income redistribution towards consumers from the US$50/bbl fall in oil prices;

- All three arrows of Abenomics shooting in the same direction, auguring continued expansion in the world’s third biggest economy.

- The unexpected Conservative Party victory in Britain—still the fifth biggest economy in the world.

Over the summer this good news was overwhelmed by the panic over China. This was not without justification. A vicious circle of devaluation, capital flight and financial distress for Chinese borrowers with US dollar liabilities could have led to contagion in other emerging economies, commodity markets and eventually the whole world financial system. But vicious circles driven by reflexive interactions between finance, economics and politics can turn suddenly into virtuous circles. If the renminbi now stabilises, with capital outflows more or less matched by China’s rising trade surplus, then the expansionary forces that drove asset prices before the summer should again become dominant—and the risk-on trades that worked so well in first half of 2015 will enjoy a comeback.

****